Output Floor Basel Iii

Https Www2 Deloitte Com Content Dam Deloitte My Documents Risk My Ra Basel Iv Placemat Pdf

Basel Iii S Final Reforms Explanation In A Nutshell Triple A Risk Finance

Overview Of Basel Iii And Related Post Crisis Reforms Executive Summary

Basel 4 Unfolds The Regulatory Challenges Continue Is Credit Risk Escaping Supervision The How And When 5 5 Treasury Insights Current Topics

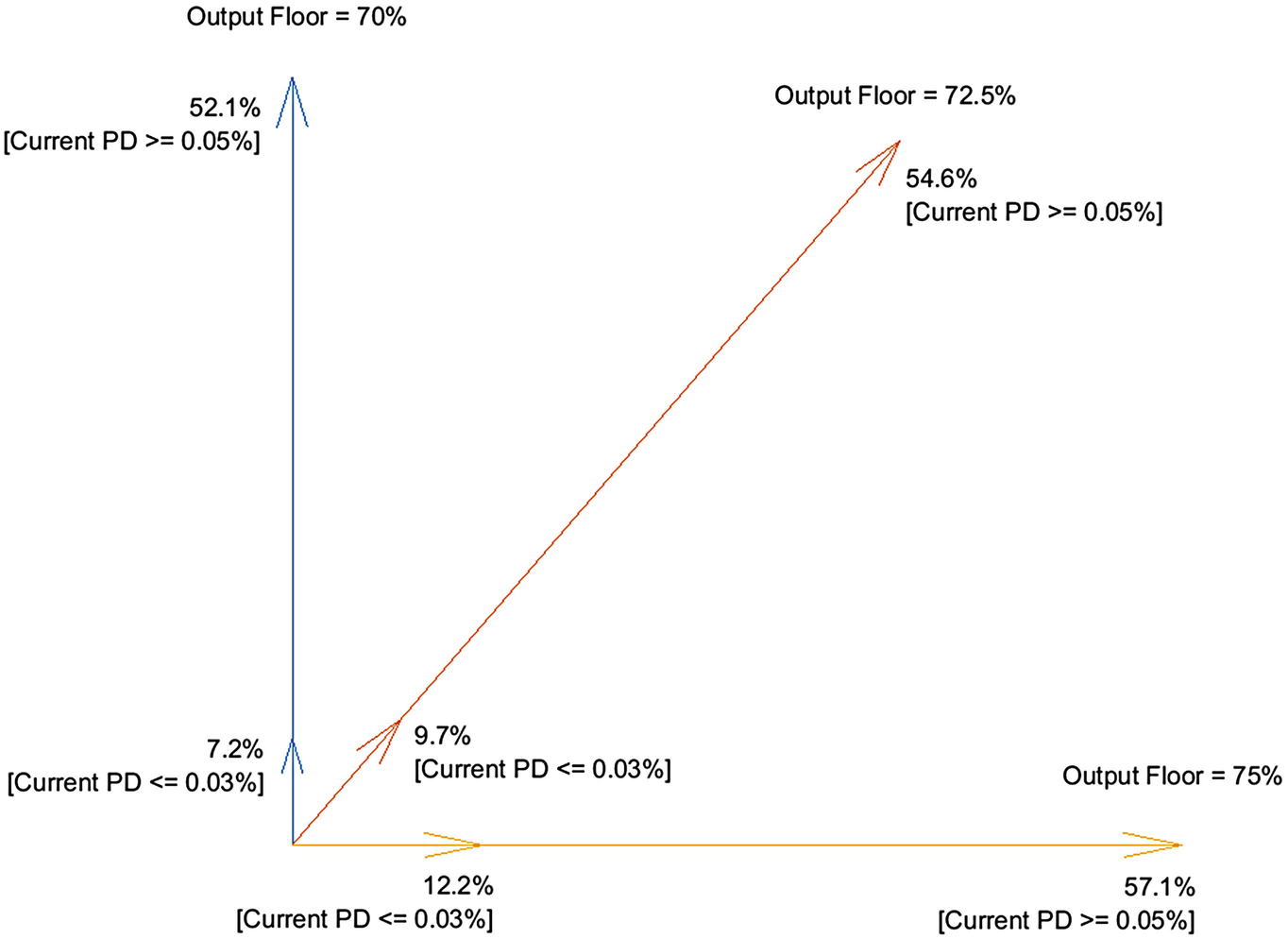

Basel Iv How Close Are The Irba Banks To The Output Floor

Https Eba Europa Eu Documents 10180 2886865 Policy Advice On Basel Iii Reforms Output Floor Pdf

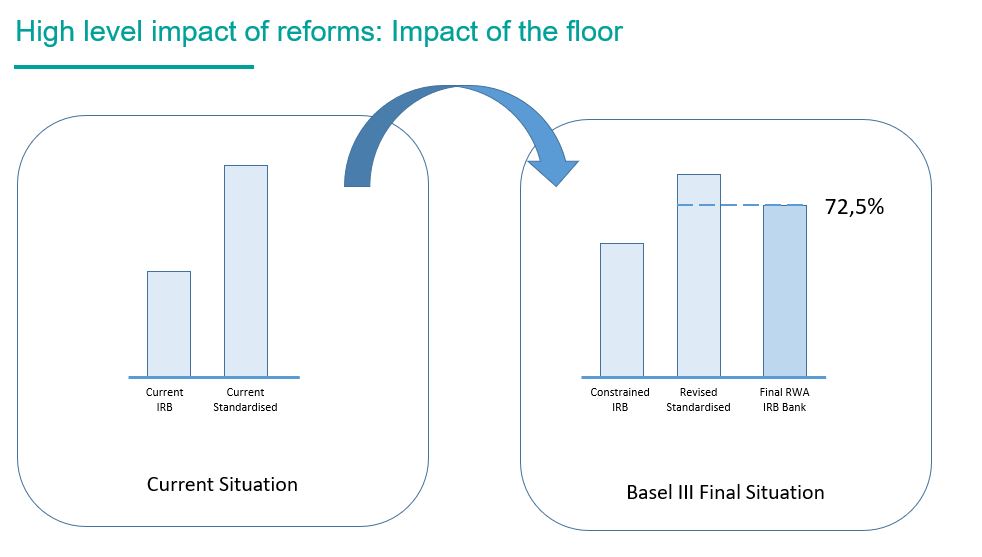

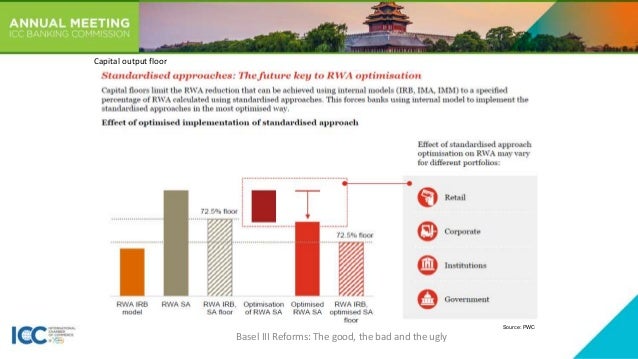

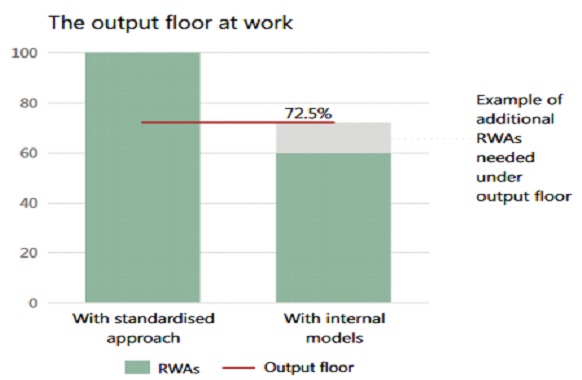

Banks calculations of rwas generated by internal models cannot in aggregate fall below 72 5 of the risk weighted assets computed by the standardised approaches.

Output floor basel iii. The most recent meeting of global regulators hashing out the revised basel iii framework once again ended in deadlock over the number intended to set a minimum proportion of risk. Trim has raised the bar for banks that use internal models. The output floor that was introduced requires that the capital requirements for. The revised output floor.

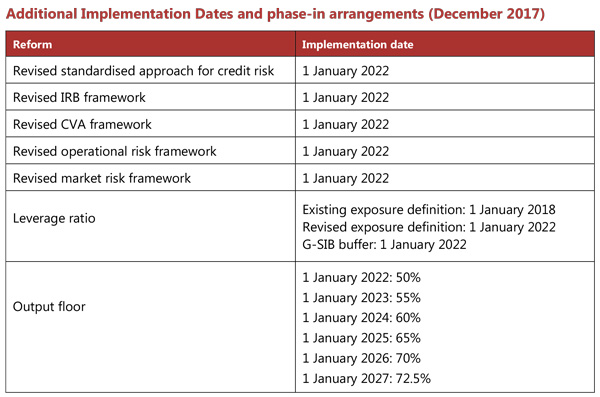

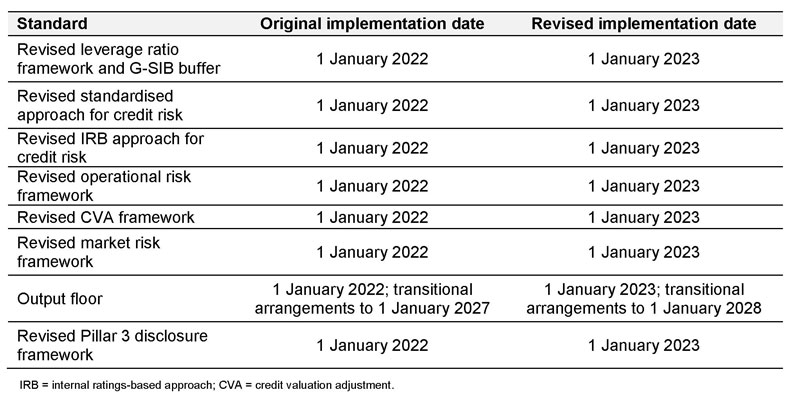

The output floor should be applied at the highest level of consolidation only. The output floor background and timeline of developments subject. The changes will occur over a transitional period from 2022 2027 basel iii basel iv. Robust risk sensitive output floor based on the revised standardised approaches.

Focus on basel output floor calibration misses the point until all the final standardised approaches are known the floor has little meaning. Among the five largest european economies spain and italy will be least affected by the reforms 1 4 and 1 5 percentage points respectively. The effect of the finalized basel iii aggregate risk weighted asset floor of 72 5 percent will therefore be a significant limit. The output floor on the other hand is part of basel iii and therefore comes from the regulatory side.

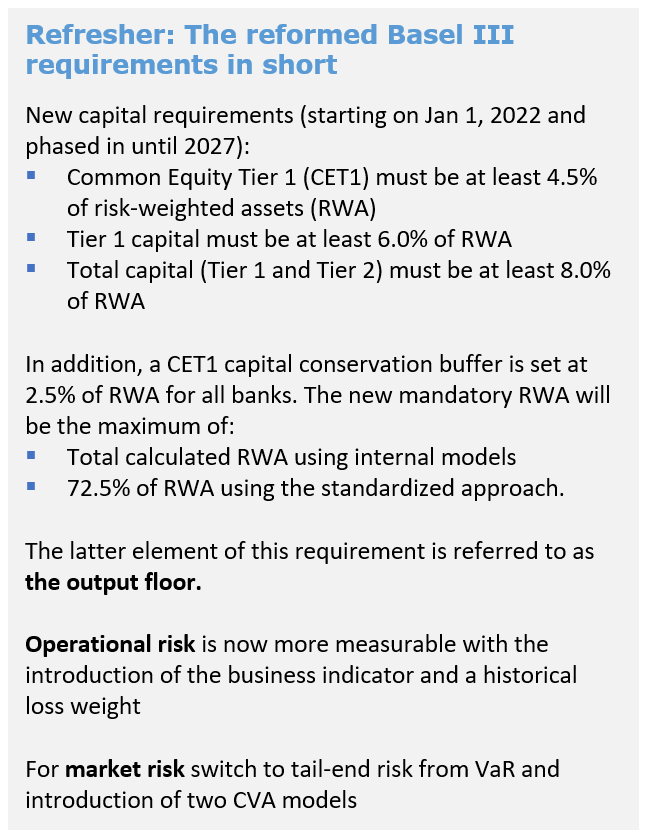

This is essential in ensuring an equilibrium in the application of basel iii as it would establish the output floor as a simple limit to the regulatory capital relief that can be achieved by using internal models while avoiding potentially adverse side effects. As set out in the basel iii framework banks must meet the following capital requirements common equity tier 1 must be at least 4 5 of risk weighted assets at all times tier 1 capital must be at least 6 0 of risk weighted assets at all times. Policy advice on the basel iii reforms. On 7 december the basel committee on banking supervision bcbs published its package of reforms known as basel iv.

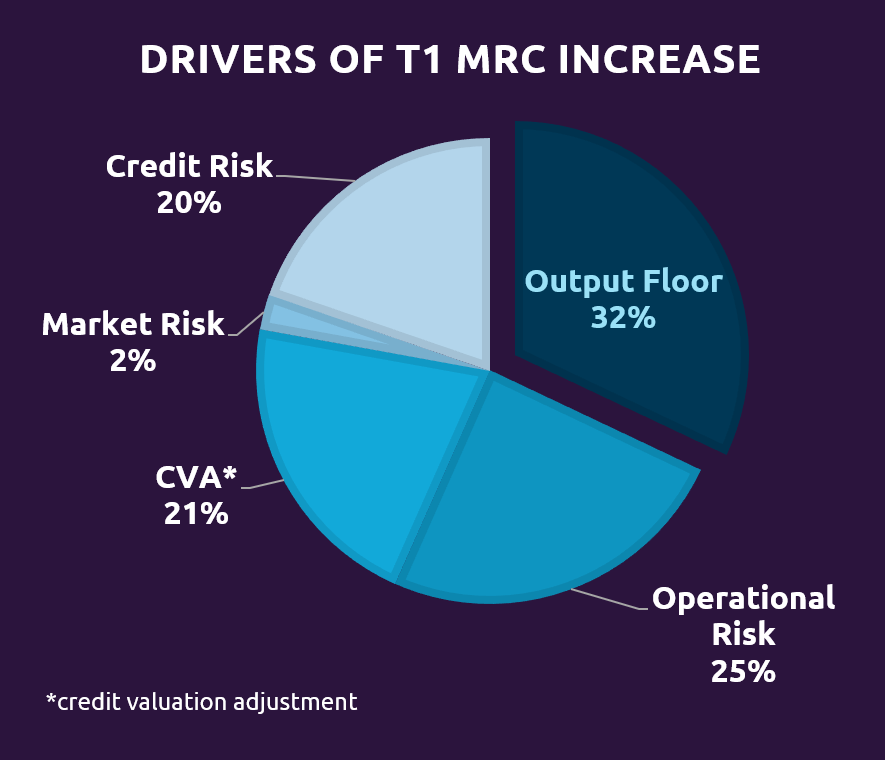

It expands the scope of the law. One of the most important and newly introduced elements of the package is the output floor designed to reduce variability in risk weighted. The basel iii output floor of when implemented in the eu through the capital requirements regulation crr3 will require risk weighted assets rwas calculated using the internal model approach to be no less than 72 5 of the rwas required under the standardised approach. In its december 2017 publication which sets out the finalisation of the basel iii framework after the crisis the basel committee introduced2 a floor requirement in the context of rwas.

Output Floor Leverage Ratio And Other Regulatory Requirements Springerlink

Box E Reforms To The Basel Iii Capital Framework Financial Stability Review April 2018 Rba

Http Www Memofin Fr Uploads Library Pdf Memo 20eba 20b C3 A2le 20contr C3 B4le 20bancaire Pdf

Https Www Bbvaresearch Com Wp Content Uploads 2017 12 Watch Basel Iv Pdf

Basel Committee Postpones Basel Iii Implementation Finadium

Basel Iii Reforms What Will Impact Banks Most

High Level Summary Of Basel Iii Reforms Better Regulation

Basel Iii The Final Regulatory Standard Mckinsey

Iii The Financial Sector Post Crisis Adjustment And Pressure Points

Bcmeeting2019 Basel Iii Reforms

Dutch Banks Unflustered By Front Loading Of Capital Rules S P Global Market Intelligence

Prudential Measures Update Wikibanks

Dutch Banks To Face Reduced Yet Still Significant Hit From Basel Iii S P Global Market Intelligence